Published on 10 February 2026

As organizations enter 2026, they continue to face an environment defined by persistent uncertainty. Multiple challenges lie ahead, from advances in artificial intelligence (AI) to evolving regulatory requirements, demanding heightened agility and oversight. The complexity of the current risk landscape presents not only challenges but also opportunities for organizations to prepare, adapt, and even get ahead. In this context, the Internal Audit Function (IAF) plays a crucial role in helping organizations turn uncertainty into informed and proactive action.

Through this article, KPMG outlines the key risk areas that may matter across your organization and recommends embedding them in your dynamic audit plan: one that integrates emerging risks while acknowledging that established threats remain highly relevant. Our aim is to provide audit functions with a clear overview of these evolving risks, along with practical considerations for how teams can respond effectively. Although the list of risks presented is not exhaustive, it offers a strong foundation from which audit functions can assess their organization’s risk profile and control environment in the period ahead.

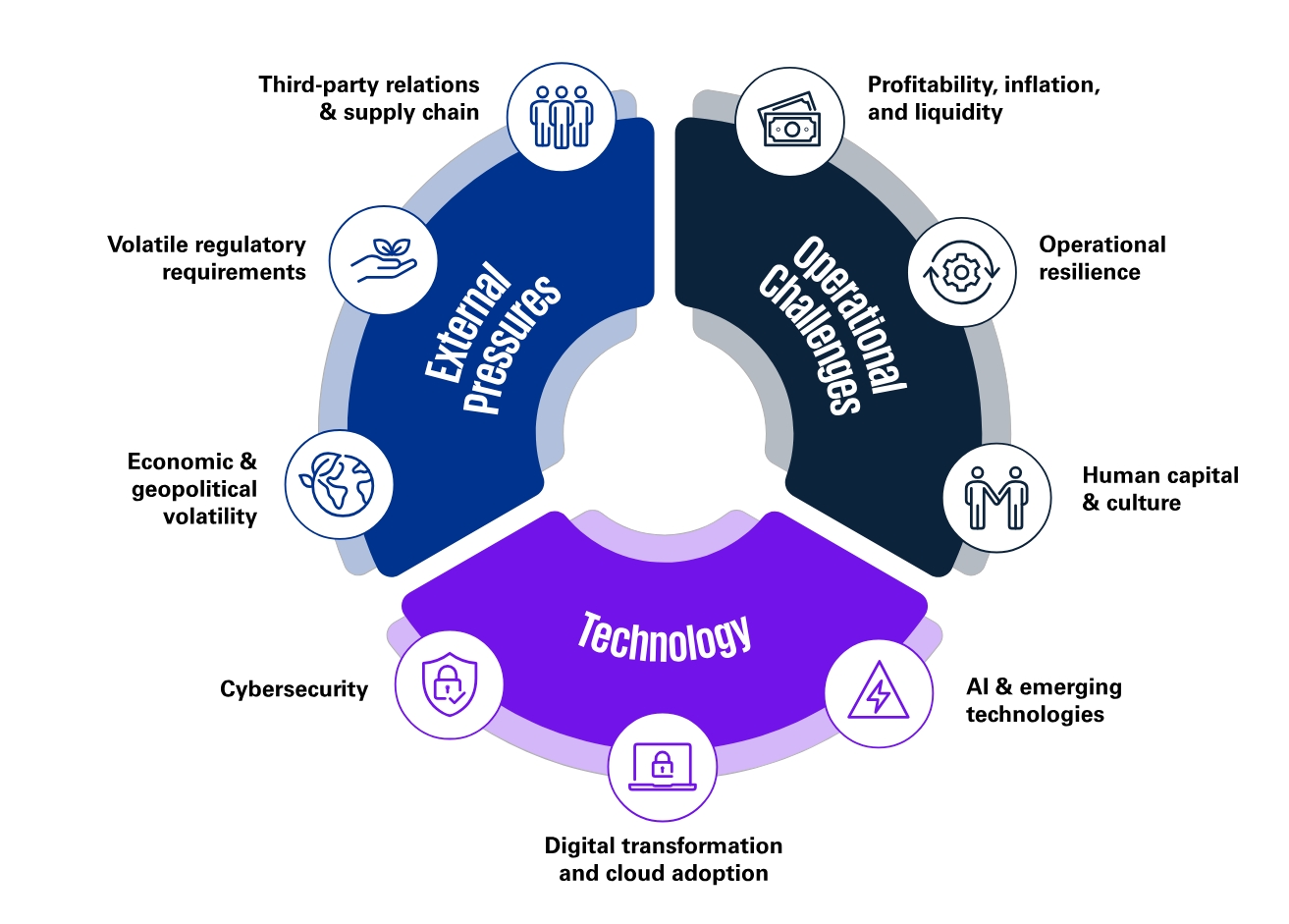

Key risks for Internal Audit in 2026

Translating the risk landscape into practical internal audit priorities requires focusing on areas where risk exposure is high and assurance adds the most value. While priorities differ by industry and organizational context, audit functions should concentrate on the most significant risks without losing sight of broader developments. With this in mind, we highlight three macro factors that should shape internal audit priorities in 2026.

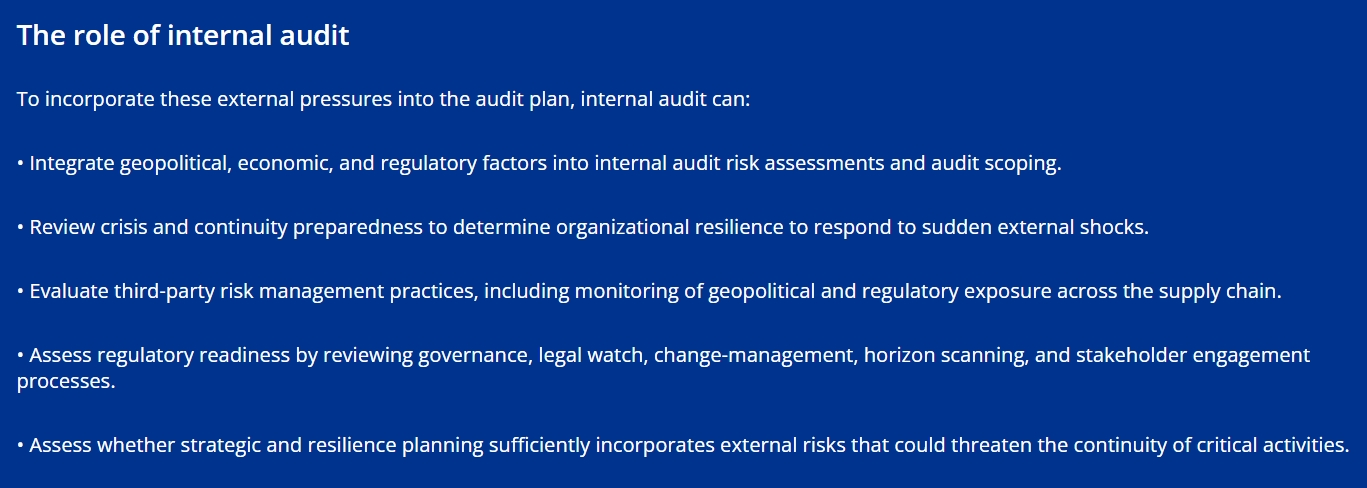

External pressures

Organizations operate in an increasingly interconnected environment where geopolitical tensions, economic uncertainty, regulatory change, and environmental risks converge, making external pressures more frequent and unpredictable. To remain resilient, organizations need agile and forward-looking risk management. In this context, internal audit should focus on external factors that can rapidly disrupt operations, strategy, and compliance. Key external pressure areas include:

Third-party relations and supply chain

Growing reliance on complex and globalized supply chains increases exposure to disruption:

- Geopolitical developments, regulatory divergence, and supplier concentration can amplify operational and compliance risks.

- Limited transparency across extended supply chains may obscure emerging vulnerabilities.

Volatile regulatory requirements

The regulatory landscape continues to expand and evolve, often across multiple jurisdictions:

- Overlapping, fast-changing, or ambiguous requirements increase compliance complexity and execution risk.

- Heightened scrutiny of governance and disclosure expectations, reinforced by new regulatory initiatives (e.g., EU Pay Transparency Directive, Critical Entities Resilience (CER) Directive, AI Act, and corporate governance codes), increases reputational and accountability risks as documentation and reporting requirements expand.

Economic and geopolitical volatility

Persistent global instability continues to affect markets, costs, and strategic assumptions.

- Energy and commodity price fluctuations, inflationary pressures, rising taxes and customs tariffs, and geopolitical conflict tensions challenge organization’s financial planning and resilience.

Strategic decisions may be based on assumptions that no longer reflect external realities.

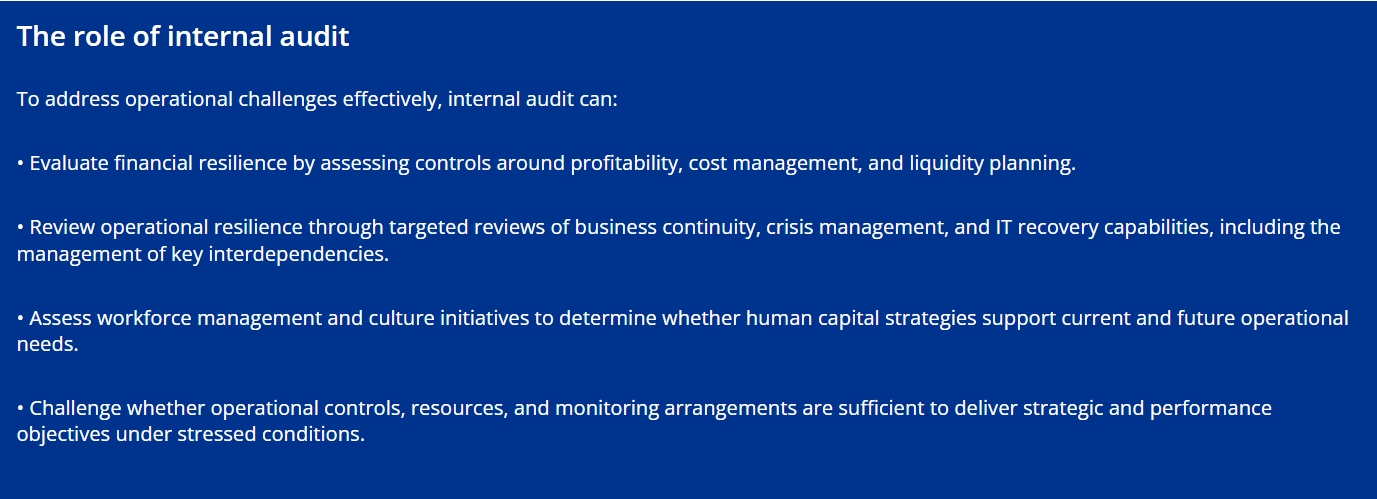

Operational challenges

Organizations face growing operational pressures driven by economic instability, rising cost pressures, and evolving workforce dynamics. These pressures increase execution risk across the operating model and require robust strategies to safeguard efficiency, resilience, and performance. Against this backdrop, internal audit should prioritize areas where operational vulnerabilities could undermine strategic objectives or financial sustainability. Key operational challenge areas include:

Profitability, inflation, and liquidity

Persistent inflation, interest rate volatility, and margin pressure heighten the risk of weakened financial resilience and constrained liquidity:

- Cost structures and pricing models may become misaligned with economic conditions.

- Liquidity buffers and funding assumptions may be insufficient under adverse scenarios.

Operational resilience

Disruptive events are becoming more frequent and complex, with impacts amplified by operational and digital interdependencies:

- Business continuity and crisis management arrangements may not fully reflect severe but plausible disruption scenarios.

- Dependence on IT systems, third parties, and shared services can create single points of failure.

Human capital and culture

Labor market constraints and changing ways of working are reshaping workforce risk:

- Talent shortages, hybrid working models, and AI-driven role changes can affect capacity, skills, and productivity.

- Misalignment between culture, incentives, and strategic priorities may weaken operational execution.

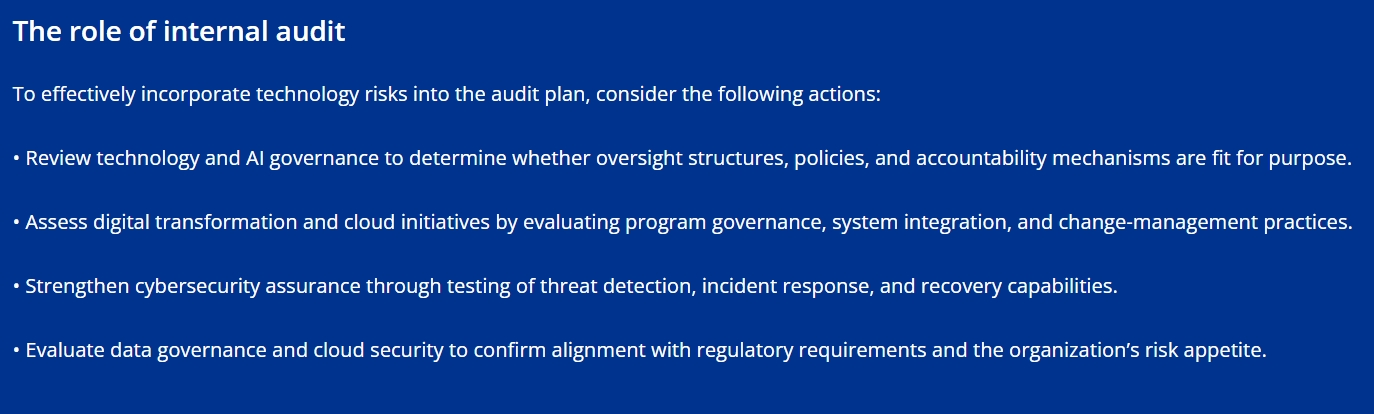

Technology

Rapid technological change continues to reshape industries, introducing both significant opportunities and heightened risks. Digital transformation, the rapid adoption of emerging technologies, and escalating cyber threats create a complex landscape in which internal audit must provide targeted and informed assurance over technology-related risks. The most relevant risk areas include:

AI and emerging technologies

The adoption of AI and other emerging technologies introduces new ethical, regulatory, and operational challenges:

- Unclear accountability, insufficient governance, or immature risk management may lead to unintended outcomes or regulatory scrutiny.

- Rapid innovation combined with decentralized system ownership, development and procurement can outpace established governance and control frameworks.

Digital transformation and cloud adoption

Large-scale digital initiatives and cloud migrations increase dependency on complex, interconnected and third-party-managed technology environments:

- Weak program governance or inadequate integration can limit value realization.

- Inconsistent security and data management practices may undermine system resilience and trust.

- High dependency on cloud providers and limited flexibility to switch or exit can jeopardize operational resilience and compliance requirements.

Cybersecurity

Cyber threats continue to intensify in scale, sophistication, and impact, with an expanding target landscape affecting organizations across all sectors.

- Ransomware, state-sponsored attacks, and vulnerabilities in legacy systems increase the risk of prolonged disruption.

- Inadequate detection, response, or recovery capabilities can significantly amplify operational, financial, and reputational damage, particularly in light of enhanced cyber resilience expectations under NIS2 and DORA.

How can KPMG help?

Effectively managing risks is essential to maintaining organizational resilience in an increasingly complex environment. KPMG supports your internal audit function by strengthening your internal audit methodology, and by translating risk landscapes into focused, executable audit plans aligned with current regulatory expectations and professional standards.

KPMG also provides hands-on support in the execution of audits by mobilizing multidisciplinary subject-matter experts across key risk domains such as governance, finance, IT and cyber, cloud and AI, regulatory compliance, and operational resilience. These specialists work alongside our internal audit teams to deliver targeted assurance, practical insights, and actionable recommendations throughout the audit process.

Through the targeted use of data analytics, technology-enabled audit techniques and proven digital tools, KPMG helps internal audit functions improve efficiency, insight, and overall assurance value.